Chapter R Reference & Sources by Chapter

Lead Teams

Chapter 4 Macro Context Refs:

•

Challenge

- How does a medium size family firm expand outside of its regional markets? Understand the challenges of internationalisation facing a medium-size family business. The case allows you to discuss the strategy of going from a local leader to a global player, the drivers of internationalisation and the logic underpinning this process, notably in an emerging market context (Latin America).

- Should the company consider scaling up its operations to other countries in the region? How should it make the transition from local leader to global actor? Evaluate the alternatives that a firm must consider when expanding to other markets. Artecola operates in Brazil, the biggest market in Latin America.

- What different entry strategies such as greenfield investment, entering equity joint- ventures, and mergers & acquisitions are available to family firms in expanding to new markets beyond the region?

- Why do family businesses in Latin America have difficulty planning long-term strategy?

Chapter 3 Macro Context Refs:

The Business of Financial Inclusion: Insights from Banks in Emerging Markets

An Evaluation of Corporate Governance Disclosure in Ghanaian and Nigerian Banks

What are the driving forces of bank competition across different income groups of countries?

West Africa's Monetary Problems

Corporate Criminal Liability – Perspectives from the US, UK and France

Corporate Criminal Liability: Call for a New Legal Regime in Nigeria

An Evaluation of Corporate Governance Disclosure in Ghanaian and Nigerian Banks

What are the driving forces of bank competition across different income groups of countries?

West Africa's Monetary Problems

Corporate Criminal Liability – Perspectives from the US, UK and France

Corporate Criminal Liability: Call for a New Legal Regime in Nigeria

Challenge

- What can we learn about emerging economies' ethics and corporate culture from this case?

- What lessons can you distil about risk management and compliance monitoring in this case

- What forward looking implications and lessons should business managers learn from this unfortunate episode?

- To what extent are companies in Nigeria seen legal persons and therefore open to criminal prosecution for acts of their agents and officers?

- Were the officers of Oceanic Bank and the various persons and companies used as fronts deserving of possible criminal prosecution?

- What roles did they play and could those roles have been described as criminal?

- * How was the former Ceo Cecilia Ibru able to get away with approving loans?

- * Was she personally behind some companies that wanted these loans? … If so, then what was the benefit for her?

- * Why did Mr. Limidu sanusi take the approach of being very outspoken about distress in the banking system?

- * Why did the former CEO Cecilia Ibru take the plea bargen? Why did the Government offered her the plea bargen?

- * The challenges the law is facing is whether her jail time was enough?

Chapter 2 Macro Context Refs:

- The Hyperglobalization of Trade and Its Future

- India's Free Trade Agreements

- International trade in goods and services in India: overview

- Indian Corporate Governance Scorecard Index

Challenge

- What was the initial reaction of Independent Directors?

- What do you think of Satyam’s decision to have backtracked its decision to invest in Maytas’ firms? Do you think it should have done this way or do you think it should have persisted with its decision?

- Why should a decision which was duly approved by the board and also ratified by the Independent Directors be reversed?

- Who was the first Independent Director to put in his paper and do you think its appropriate?

- The board meeting was called for December 29th 2008 and it was postponed to January 10th 2009 only to accommodate and have the presence of its Independent Directors. However, the case indicates that three of its Independent Directors resigned on January 2nd 2009. Was it right on their part to done so?

- Having done so, were the Independent Directors disowning their responsibility? Was it not also their responsibility to explain their stand and circumstances which force them to ratify the decision to invest in Maytas’ firms?

- As the investors continue to resist the outside influences, it adds some more doubts on various issues among the global intelligentsia. They are: Is there any need to curb the influence exerted by institutional investors, hedge funds and mutual funds (the main perpetrators of the 2008 US Financial Crisis) which have been replacing insurance companies and pension funds in the investment activities? Should the market be kept under strict control with iron hand? Is a viable code of conduct required? If so, what kind of model should be followed, either US, UK, Germany, etc., or is there any need for a common code of conduct at the global level and who should be given the authority to execute this code?

- 1. How someone is supposed to invest in an industry whose financial statements do not reflect the economic reality?

2. What steps can the company follow to provide reliability and transparency to the investors?

3. How can corruption risk and non-ethical behaviours from the managers/board be mitigated?

Investment Teams

Chapter 4 Meso & Micro Context Refs

Challenge

- If Artecola were to move away from their traditional portfolio range and beyond Latin America what countries and industries could they adapt to and why?

- With increased levels of debt (to a suitable level) Artecola would need to ensure this doesn’t increase to any further levels, how would you suggest they raise the capital for any future FDI.

Chapter 3 Meso & Micro Context Refs:

Nigeria: Finding opportunities where others fear to tread

Challenge

- Should Cecilia Ibru have been denied a plea bargain?

- Is there any big lesson about strategy for handling accusation of business crimes based on Mrs. Ibru’s approach in this case?

- How much did other top management staff know about the profit management and cover‐up?

- How does the above effect investment decision in the Nigerian Banking sector today?

- What discount rate would you expect to pay for investing in the Nigerian Commercial Banking sector that allows for the above risks to be integrated

- Who should be interested in investing in the Nigerian Commercial Banking sector? Why and a what justified valuations?

Chapter 2 Meso & Micro Context Refs:

- The Information and Communication Technology Sector in India

- Maytas, Hyderabad Metro andthe Politics of Real Estate

- Telecom Regulatory and Policy Environment in India

Challenge

- Was the Satyam Computer Services Ltd.’s decision to invest/acquire 51% stake in Maytas Infra and 100% stake in Maytas Properties – a bad decision or a wrong decision?

- Why did the investors react so violently and vehemently to the decision by knocking down 57% off Satyam's market-cap on NYSE on December 17th 2008?

- How did the market react to Satyam’s decision to invest in CEO’s son’s firm and how did the foreign bourses react to the same decision?

- Would Indian markets have reacted in the same way as they did if the US markets would not have reacted the way they did?

- What was the immediate reaction of Satyam to the market reaction?

- What was the initial reaction of Independent Directors?

- Base on the above should our international investment fund revisit the Indian ICT sector or not? and which companies and why?

Action teams

Chapter 3

Ed's Notes:

Learning outcomes (with references) post-MICA:

- The case also exposed the Achilles heel of failure in implementation of the banking consolidation policy of CBN. One of the objectives was to rid the industry of so called ‘Papa and mama’ banks (closely held banks) because of the poor implications for corporate governance.

- Accomplices in the commission of an offence can end up being charged as principal offenders.

- Cooperation with law enforcement authorities is a wise step in cases that are ‘unwinnable’, as a contrary approach tends to lead them to a conclusion that the accused person is not remorseful and is not deserving of any leniency.

- Where a business organization is involved, it should decide strategy based on the need to ‘ring fence’ the crime of its officers and to minimize disruption of its business.

- Each director is individually bound to meet high standards of diligence and to be subject to civil liability under the Companies and Allied Matters Act for breach of director’s duties for the general failings of the entire Board, regardless of the individual’s active participation.

- Lax ethical standards, lack of processes and procedures for compliance and risk management, lack of a truth telling culture that allows honest mistakes, over‐ambitious growth and performance targets, greed, poor internal controls and outsize egos may lead to that first step that is meant to be ‘temporary’ but tends to grow out of control into a monster that transforms ‘amiable’ and ‘harmless’ managers into apparent titans of corruption and criminality.

- Effective Board oversight, whistle‐blowing structures and a culture of integrity and excellence are required, but implementation will always remain a challenge and a test for character. Astute regulatory oversight is equally required.

Chapter 2

Ed's Notes:Learning outcomes (with references) post-MICA:

- The failure of capital markets to fairly value an Indian multinational because of state involvement and auditors' malpractice. And how a (local) government contract in an unrelated business can be detrimental to normal market functioning and efficiencies

- How the G-overnance in ESG is the major hurdle that international investors face when considering emergent markets

- How CSV (Porter, M) might be a better criteria than CSR within which to situate brand and related corporate valuation of an emerging market company

- The benefits of emerging enterprises listing on international stock exchanges as they require greater discipline, oversight, compliance and transparency in ownership and governance rules: "disclosure among listed companies via voluntary guidance, listing rules, and training activities." plus"some stock exchanges have programmes to help SMEs to develop their management capacity, strengthen their governance structures and innovate and grow."

- The opacity of compliance enforcement at national institutional levels- in this case India

General & Supporting Readings resources

Innovation in EMs:

Innovation in EMs:

•Autor, David, David Dorn, and Gordon Hanson

(2013). “The China Syndrome: Local Labor Market Effects of Import Competition

in the United States”, American Economic Review.

103(6): 2121–2168.

•Rapoza, Kenneth (2011). “Is China Bad For The U.S. Job Market?” Forbes. August 22, 2011. http://www.forbes.com/sites/kenrapoza/2011/08/22/is-china-bad-for-the-us-job-market/

•Runjuan Liu, Daniel Trefler (2008). “Much Ado About Nothing: American Jobs and the Rise of Service Outsourcing to China and India”, NBER Working Paper No. 14061. June 2008.

•Scott, Robert and Will Kimball (2014). “China Trade, Outsourcing and Jobs”, Briefing Paper #385. Economic Policy Institute. http://s2.epi.org/files/2014/bp385-china-trade-deficit.pdf

•Buckley, Peter, (2011). “International Integration and Coordination in the Global Factory”, Management International Review. 51:269–283.

•Dawar, N. and Frost, T. (1999), “Competing with giants: survival strategies for local companies in emerging markets”, Harvard Business Review, Vol. 77, pp. 119-132.

•OECD-WTO-UNCTAD. (2013). Implications of global value chains for trade, investment, development and jobs. Report Prepared for the G-20 Leaders Summit, September. http://unctad.org/en/PublicationsLibrary/unctad_oecd_wto_2013d1_en.pdf .

•UNCTAD. 2013. World Investment Report 2013: Global value chains: Investment and Trade for Development. New York: United Nations. http://unctad.org/en/PublicationsLibrary/wir2013_en.pdf

•Yeung, Henry Wai-chung, and Neil Coe, (2014).“Toward a Dynamic Theory of Global Production Networks”, Economic Geography. 91(1):29–58.

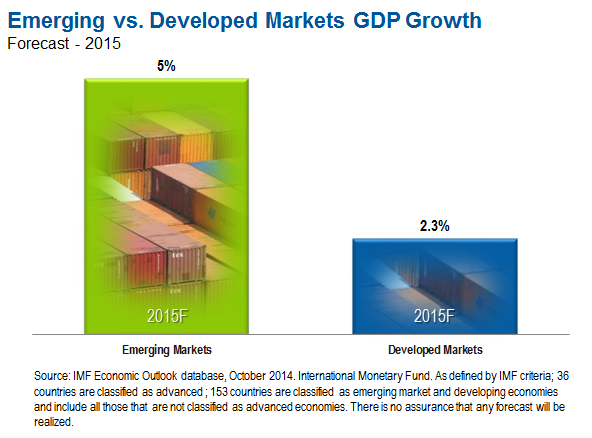

• IMF forecast for 2015: http://mobius.blog.franklintempleton.com/wp-content/uploads/2014/12/2015_EMGDPForecast.png

•Egan, Henry, and Armen Ovanessoff, (2011). “Capturing the Growth Opportunity in Emerging Markets”, The European Business Review. November. http://www.europeanbusinessreview.com/?p=3301

•Emerging markets can be seen as locations for production, because of their low costs. The costs can be compared in general, using the Economist’s Big Mac index that comes out every July and occasionally in January. The index shows the price of a Big Mac hamburger in about 50 countries, demonstrating where prices are lower (most of emerging Asia) and where they are high (Scandinavia and Switzerland) http://www.economist.com/content/big-mac-index

•Another useful measure of low costs in emerging markets is wage information. The US Bureau of Labor Statistics has compiled a comparison of manufacturing wages http://www.bls.gov/fls/#compensation

•Bell, David, and Mary Shelman, (2011). “KFC’s Radical Approach to China”, Harvard Business Review. 89: No 11. November. pp. 1-6.

•Gupta, Sudheer and Daniel Shapiro, (2014). “Building and Transforming an Emerging Market Global Enterprise: Lessons from the Infosys Journey”, Business Horizons. Vol 57. pp. 169-179.

•

•Ricart, Joan, and Pablo Agnese, “Adding Value through Offshoring”, (2011). IESE Insight Magazine. Issue 10, 3rd Quarter.

International Monetary Fund 2014) World economic outlook database (October) [online] http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/weoselco.aspx?g=2001&sg=All+countries

•Marta NEÈADOVÁ and Hana SCHOLLEOVÁ, (2011). “Competitiveness and Innovation Performance of the Czech Republic in International Rankings”, Research Journal of Economics, Business and ICT. Vol 4. [ojs.journals.cz/index.php/RJEBI/article/download/248/252]

•

•McKinsey Global Institute (2012). The Archipelago Economy: Unleashing Indonesia’s Potential. Boston: McKinsey & Company.

•Deloitte (2015). Competitiveness: Catching the Next Wave, Mexico. https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-gbc-mexico-competitiveness-report-english.pdf

•Christensen, Clayton, (2001). “The Past and Future of Competitive Advantage”, Sloan Management Review. Vol. 42, No. 2. (Winter). pp. 105-109.

•Economist (2015). What China Wants. Economist, http://www.economist.com/news/essays/21609649-china-becomes-again-worlds-largest-economy-it-wants-respect-it-enjoyed-centuries-past-it-does-not

•International Monetary Fund 2014) World economic outlook database (October) [online] http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/weoselco.aspx?g=2001&sg=All+countries

•Jones, G and Khanna, T (2006). “Bringing history (back) into international business”, Journal of International Business Studies, 37, pp 453-468.

•Jones, G. (2000). Merchants to Multinationals. Oxford: Oxford University Press.

••Khanna, Tarun, and Krishna Palepu (2010). Winning in Emerging Markets: A Road Map for Strategy and Execution. Cambridge, Mass.: Harvard Business School Press.

•Harvard Business Review, ed. (2011). Thriving in Emerging Markets. Cambridge, Mass.: Harvard Business School Press.

•Bhattacharya, Arindam K. and David Michael (2008). “How Local Companies Keep Multinationals at Bay”, Harvard Business Review, March. pp. 84-95.

•Bell, David, and Mary Shelman, (2011). “KFC’s Radical Approach to China”, Harvard Business Review. 89: No 11. November. pp. 1-6.

•Choudhary, Vimal, Martin Dewhurst, and Alok Kshirsagar (2012). “How Western Multinationals can Organize to win in Emerging Markets”, McKinsey Quarterly.

•Hansen, Michael, Marcus Larsen, Torben Pedersen, Bent Petersen, and Peter Wad (2010). Strategies in Emerging Markets: A Case Book on Danish Multinational Corporations in China and India. Copenhagen: Copenhagen Business School Press. September 1.

•Stanford Graduate School of Business, (2014). “The Chinese Wireless Communications Industry in 2012 and Beyond: An Industry Note”. Case #SM227.

•KPMG (2014). Mainland China Banking Survey 2014. https://www.kpmg.com/CN/en/IssuesAndInsights/ArticlesPublications/Documents/Mainland-China-Banking-Survey-201411.pdf

•Niedermeyer, Edward (2014). “How China Protects Its Auto Industry”, BloombergView. August 15. http://www.bloombergview.com/articles/2014-08-15/how-china-protects-its-auto-industry

•Grosse, Robert (forthcoming 2016). “How Emerging Markets Firms will Become Global Leaders”, International Journal of Emerging Markets.

•Guillen, M. F., & Garcia-Canal, E. (2009). “The American model of the multinational firm and the ‘new’ multinationals from emerging economies”, Academy of Management Perspectives, 23(2), 23—35.

•Ramamurti, Ravi (2012). “What is Really Different about Emerging Market Multinationals?” Global Strategy Journal. Vol. 2, pp. 42-47.

•Demirbag, Mehmet, and Attila Yaprak (eds.) (2015). Handbook of Emerging Market Multinational Corporations. Camberley, Surrey, UK: Edward Elgar Publishing.

•Ramamurti, Ravi (2012). “Competing with Emerging Market Multinationals”. Business Horizons. Vol 55. pp. 241-249.

•Chattopadhyay, Amitava, and Rajeev Batra (2012). The New Emerging Market Multinationals: Four Strategies for Disrupting Markets and Building Brands. New York: McGraw-Hill.

•Richard Dobbs et al. (2013). “Urban world: The shifting global business landscape”, McKinsey Quarterly. October. http://www.mckinsey.com/insights/urbanization/urban_world_the_shifting_global_business_landscape

•Boston Consulting Group, (2014). BCG Challengers 2014: Redefining Global Competitive Dynamics. Boston: BCG. September. http://www.aicb.org.my/wp-content/uploads/2013/03/Redefining_Global_Competitive_Dynamics_Sep_2014.pdf

•Chattopadhyay, Amitava, and Rajeev Batra (2012). The New Emerging Market Multinationals: Four Strategies for Disrupting Markets and Building Brands. New York: McGraw Hill.

•Economist (2008). “Emerging Market Multinationals: The Challengers”, The Economist. January 10. http://www.economist.com/node/10496684

•Guillen, M, and Garcia-Canal, E (2012). Emerging markets rule: Growth strategies of the new global giants, McGraw-Hill, New York.

•Ramamurti, Ravi and Jitendra Singh (2010). Emerging Multinationals in Emerging Markets. Cambridge, UK: Cambridge University Press.

•Sauvant, K (2008). The rise of transnational corporations from emerging markets. Cheltenham, Surrey, UK: Edward Elgar.

•Xu, M (2010). Foxconn Truth. Hangzhou, China: Zhejiang University Press. (in Chinese)

•Rapoza, Kenneth (2011). “Is China Bad For The U.S. Job Market?” Forbes. August 22, 2011. http://www.forbes.com/sites/kenrapoza/2011/08/22/is-china-bad-for-the-us-job-market/

•Runjuan Liu, Daniel Trefler (2008). “Much Ado About Nothing: American Jobs and the Rise of Service Outsourcing to China and India”, NBER Working Paper No. 14061. June 2008.

•Scott, Robert and Will Kimball (2014). “China Trade, Outsourcing and Jobs”, Briefing Paper #385. Economic Policy Institute. http://s2.epi.org/files/2014/bp385-china-trade-deficit.pdf

•Buckley, Peter, (2011). “International Integration and Coordination in the Global Factory”, Management International Review. 51:269–283.

•Dawar, N. and Frost, T. (1999), “Competing with giants: survival strategies for local companies in emerging markets”, Harvard Business Review, Vol. 77, pp. 119-132.

•OECD-WTO-UNCTAD. (2013). Implications of global value chains for trade, investment, development and jobs. Report Prepared for the G-20 Leaders Summit, September. http://unctad.org/en/PublicationsLibrary/unctad_oecd_wto_2013d1_en.pdf .

•UNCTAD. 2013. World Investment Report 2013: Global value chains: Investment and Trade for Development. New York: United Nations. http://unctad.org/en/PublicationsLibrary/wir2013_en.pdf

•Yeung, Henry Wai-chung, and Neil Coe, (2014).“Toward a Dynamic Theory of Global Production Networks”, Economic Geography. 91(1):29–58.

• IMF forecast for 2015: http://mobius.blog.franklintempleton.com/wp-content/uploads/2014/12/2015_EMGDPForecast.png

•Egan, Henry, and Armen Ovanessoff, (2011). “Capturing the Growth Opportunity in Emerging Markets”, The European Business Review. November. http://www.europeanbusinessreview.com/?p=3301

•Emerging markets can be seen as locations for production, because of their low costs. The costs can be compared in general, using the Economist’s Big Mac index that comes out every July and occasionally in January. The index shows the price of a Big Mac hamburger in about 50 countries, demonstrating where prices are lower (most of emerging Asia) and where they are high (Scandinavia and Switzerland) http://www.economist.com/content/big-mac-index

•Another useful measure of low costs in emerging markets is wage information. The US Bureau of Labor Statistics has compiled a comparison of manufacturing wages http://www.bls.gov/fls/#compensation

•Bell, David, and Mary Shelman, (2011). “KFC’s Radical Approach to China”, Harvard Business Review. 89: No 11. November. pp. 1-6.

•Gupta, Sudheer and Daniel Shapiro, (2014). “Building and Transforming an Emerging Market Global Enterprise: Lessons from the Infosys Journey”, Business Horizons. Vol 57. pp. 169-179.

•

•Ricart, Joan, and Pablo Agnese, “Adding Value through Offshoring”, (2011). IESE Insight Magazine. Issue 10, 3rd Quarter.

International Monetary Fund 2014) World economic outlook database (October) [online] http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/weoselco.aspx?g=2001&sg=All+countries

•Marta NEÈADOVÁ and Hana SCHOLLEOVÁ, (2011). “Competitiveness and Innovation Performance of the Czech Republic in International Rankings”, Research Journal of Economics, Business and ICT. Vol 4. [ojs.journals.cz/index.php/RJEBI/article/download/248/252]

•

•McKinsey Global Institute (2012). The Archipelago Economy: Unleashing Indonesia’s Potential. Boston: McKinsey & Company.

•Deloitte (2015). Competitiveness: Catching the Next Wave, Mexico. https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-gbc-mexico-competitiveness-report-english.pdf

•Christensen, Clayton, (2001). “The Past and Future of Competitive Advantage”, Sloan Management Review. Vol. 42, No. 2. (Winter). pp. 105-109.

•Economist (2015). What China Wants. Economist, http://www.economist.com/news/essays/21609649-china-becomes-again-worlds-largest-economy-it-wants-respect-it-enjoyed-centuries-past-it-does-not

•International Monetary Fund 2014) World economic outlook database (October) [online] http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/weoselco.aspx?g=2001&sg=All+countries

•Jones, G and Khanna, T (2006). “Bringing history (back) into international business”, Journal of International Business Studies, 37, pp 453-468.

•Jones, G. (2000). Merchants to Multinationals. Oxford: Oxford University Press.

••Khanna, Tarun, and Krishna Palepu (2010). Winning in Emerging Markets: A Road Map for Strategy and Execution. Cambridge, Mass.: Harvard Business School Press.

•Harvard Business Review, ed. (2011). Thriving in Emerging Markets. Cambridge, Mass.: Harvard Business School Press.

•Bhattacharya, Arindam K. and David Michael (2008). “How Local Companies Keep Multinationals at Bay”, Harvard Business Review, March. pp. 84-95.

•Bell, David, and Mary Shelman, (2011). “KFC’s Radical Approach to China”, Harvard Business Review. 89: No 11. November. pp. 1-6.

•Choudhary, Vimal, Martin Dewhurst, and Alok Kshirsagar (2012). “How Western Multinationals can Organize to win in Emerging Markets”, McKinsey Quarterly.

•Hansen, Michael, Marcus Larsen, Torben Pedersen, Bent Petersen, and Peter Wad (2010). Strategies in Emerging Markets: A Case Book on Danish Multinational Corporations in China and India. Copenhagen: Copenhagen Business School Press. September 1.

•Stanford Graduate School of Business, (2014). “The Chinese Wireless Communications Industry in 2012 and Beyond: An Industry Note”. Case #SM227.

•KPMG (2014). Mainland China Banking Survey 2014. https://www.kpmg.com/CN/en/IssuesAndInsights/ArticlesPublications/Documents/Mainland-China-Banking-Survey-201411.pdf

•Niedermeyer, Edward (2014). “How China Protects Its Auto Industry”, BloombergView. August 15. http://www.bloombergview.com/articles/2014-08-15/how-china-protects-its-auto-industry

•Grosse, Robert (forthcoming 2016). “How Emerging Markets Firms will Become Global Leaders”, International Journal of Emerging Markets.

•Guillen, M. F., & Garcia-Canal, E. (2009). “The American model of the multinational firm and the ‘new’ multinationals from emerging economies”, Academy of Management Perspectives, 23(2), 23—35.

•Ramamurti, Ravi (2012). “What is Really Different about Emerging Market Multinationals?” Global Strategy Journal. Vol. 2, pp. 42-47.

•Demirbag, Mehmet, and Attila Yaprak (eds.) (2015). Handbook of Emerging Market Multinational Corporations. Camberley, Surrey, UK: Edward Elgar Publishing.

•Ramamurti, Ravi (2012). “Competing with Emerging Market Multinationals”. Business Horizons. Vol 55. pp. 241-249.

•Chattopadhyay, Amitava, and Rajeev Batra (2012). The New Emerging Market Multinationals: Four Strategies for Disrupting Markets and Building Brands. New York: McGraw-Hill.

•Richard Dobbs et al. (2013). “Urban world: The shifting global business landscape”, McKinsey Quarterly. October. http://www.mckinsey.com/insights/urbanization/urban_world_the_shifting_global_business_landscape

•Boston Consulting Group, (2014). BCG Challengers 2014: Redefining Global Competitive Dynamics. Boston: BCG. September. http://www.aicb.org.my/wp-content/uploads/2013/03/Redefining_Global_Competitive_Dynamics_Sep_2014.pdf

•Chattopadhyay, Amitava, and Rajeev Batra (2012). The New Emerging Market Multinationals: Four Strategies for Disrupting Markets and Building Brands. New York: McGraw Hill.

•Economist (2008). “Emerging Market Multinationals: The Challengers”, The Economist. January 10. http://www.economist.com/node/10496684

•Guillen, M, and Garcia-Canal, E (2012). Emerging markets rule: Growth strategies of the new global giants, McGraw-Hill, New York.

•Ramamurti, Ravi and Jitendra Singh (2010). Emerging Multinationals in Emerging Markets. Cambridge, UK: Cambridge University Press.

•Sauvant, K (2008). The rise of transnational corporations from emerging markets. Cheltenham, Surrey, UK: Edward Elgar.

•Xu, M (2010). Foxconn Truth. Hangzhou, China: Zhejiang University Press. (in Chinese)

{kind=link}

Comments

Post a Comment